Many of us are feeling overwhelmed in these times of economic uncertainty. With lockdown restrictions, many of us have suffered a shortfall in earnings or worse.

Perhaps you find yourself struggling to pay off your various credit cards or loans. If your answer is “yes”, you can seek debt consolidation for good or bad credit.

What is Debt Consolidation?

A debt consolidation loan is a loan taken out to cover your existing high-interest credit, such as store accounts and credit card debt. Consolidation loans are usually taken out over longer terms and carry a lower interest rate.

Once a borrower has consolidated his or her debt, the repayment process becomes streamlined into one monthly payment, which can save you money on administration fees and cut down on other headaches.

Can You Get a Debt Consolidation Loan for Good or Bad Credit?

Generally, a credit score follows the FICO (Fair Isaac Corporation) model that rates a potential borrower’s creditworthiness on a three-digit rating from 300 to 850.

According to FICO, the ratings are as follows:

- Fair credit rating 580 to 669

- Poor Credit rating 300 to 579

- Good Credit rating 670 to 739

Borrowers with good credit scores have open options to approach the traditional banking system and will typically be offered lower interest repayments on a consolidation loan.

Know Your Credit Score

When applying for a consolidation loan for good or bad credit, it is always best to request a credit score report. Many banks offer this service for free (be aware that too many “hard credit checks” by institutions can lower your credit score).

Options for Consolidation Loans with a Poor Credit Score

When seeking a consolidation loan for a good or poor credit score, it is best to compare options from a variety of lenders: local banks, online lenders, and credit unions.

Online lenders are an excellent alternative to the traditional banking system because they often provide credit score minimums and conduct “soft credit checks” that will not affect your credit score.

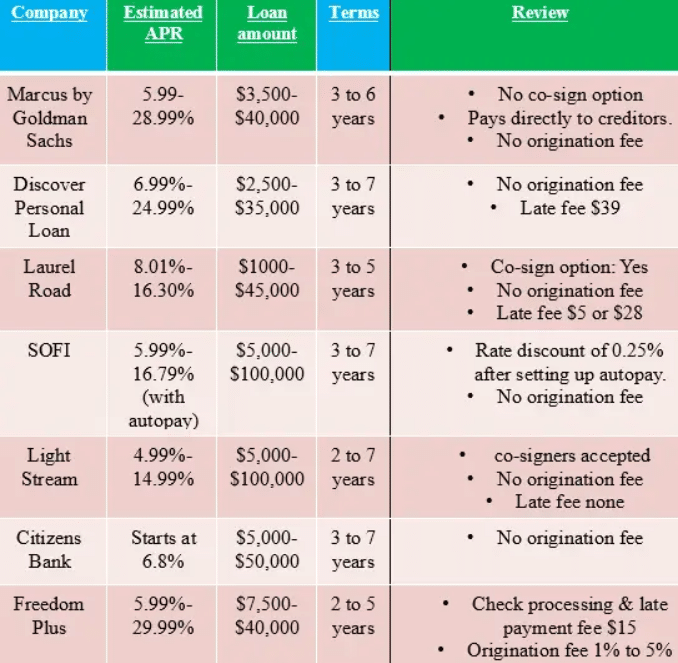

When comparing potential consolidation loans, be sure to calculate the APR (Annual Percentage Rate), which includes hidden costs such as penalties as well as calculating other costs like origination fees.

Secured Loan Options

If you are having difficulty finding a good value, unsecured consolidation loan for good or bad credit, you may choose to apply for a secured loan.

Most consolidation loans are unsecured, which means that the lender’s risk increases and the interest of the loan rise accordingly.

Secured loans require that the borrower provides collateral in the form of a high-value asset such as a car or home. Because this type of loan is secured, there is less risk to the lender, and you generally will receive a lower interest rate. Secured loans also have a high approval rate, even for those with poor credit scores.

What Are the Advantages of a Consolidation loan?

When a consumer has multiple accounts, it can make payments each month time consuming and complicated. Once you consolidate your debt, you only need to make one payment per month. You are also less likely to skip or make a late payment, which can occur when juggling multiple installments a month.

When you consolidate your debt, you can pay back your debt over terms with a lower overall interest rate, so you end up paying less over the repayment period.

Where to Apply for Consolidation Loans for Good or Bad Credit

Credit Unions and Local Banks

If you are a customer of a local bank or a credit union member, you may approach them directly for a consolidation loan. These institutions may have a positive history with you and be willing to overlook your poor credit scores. In these cases, your employment and monthly earnings may factor in their approval for a consolidation loan.

Online Lenders

Online lenders allow borrowers to shop around for loans without the “hard credit checks” that bring their credit scores down. Approval time is short, and you may receive the funds much more quickly than in the lengthy procedures of the traditional banking system.

Some online lenders claim they guarantee approval, but this is not entirely true, even if most online lenders will overlook a poor credit score. Legitimate lenders will need you to provide proof of income and employment to exercise due diligence.

Some experts suggest that borrowers avoid third party lenders and approach direct lenders themselves to avoid added costs.

How to Manage Your Consolidation Loan

If your lender approves your consolidation loan application, make sure that you know your financial status thoroughly. It is essential to factor in your total debts, monthly expenses, and monthly income to be sure that you can afford to pay off your consolidation loan.

Beware of unscrupulous online lenders and read through your contracts for any fine print penalties and hidden costs. Once approved, be diligent in paying off your consolidation loan on time and in full. This good payment record will increase your credit rating and open other doors if you need a loan in the future.